TIME

Forecasted timings.

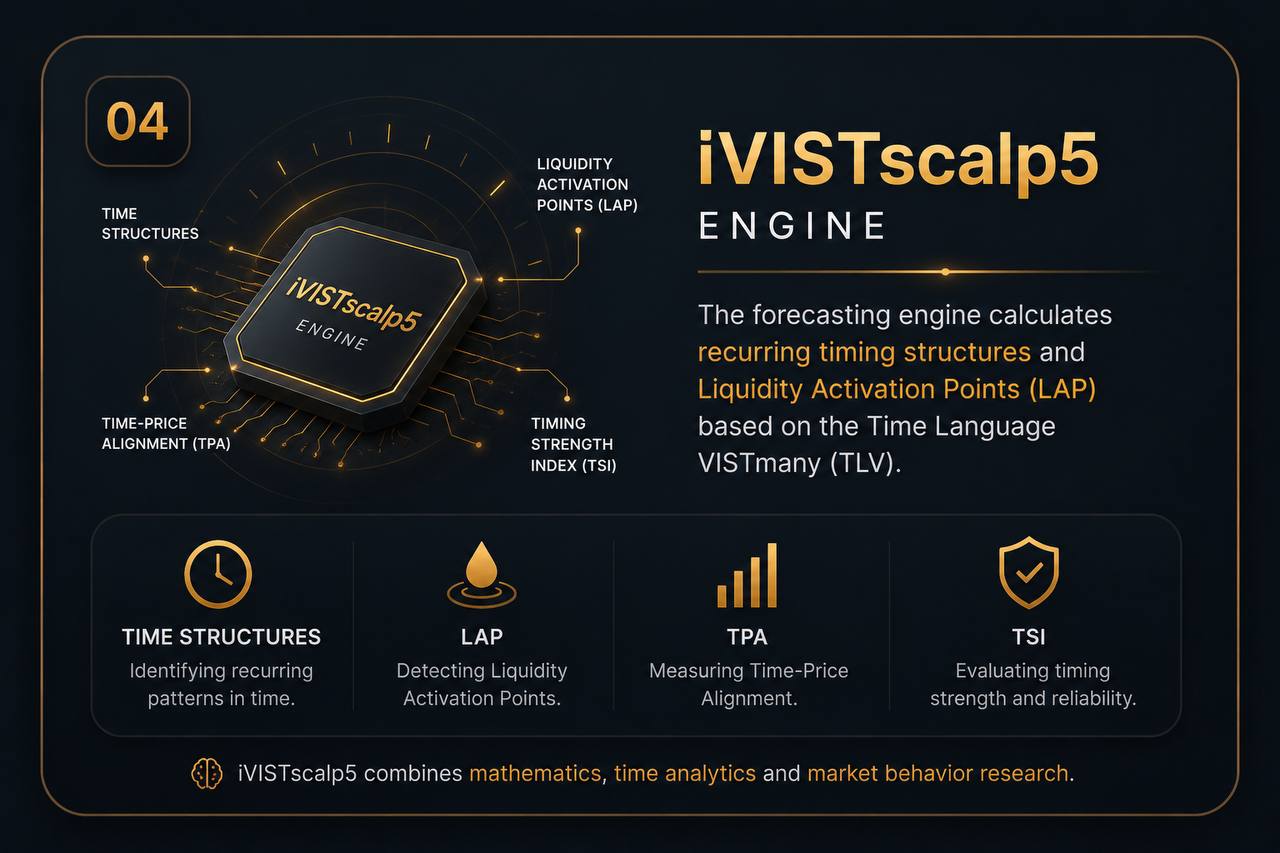

Liquidity Activation Points (LAP).

Forecasted timings.

Liquidity Activation Points (LAP).

Reaction levels.

Time-Price Alignment (TPA).

Market activation.

Momentum Clusters.

Timing Strength Index (TSI).

Trading decisions.

High-probability timing execution.

The market moves when time activates price

TLV • LAP • TPA • TSI

MARKETS COVERED

•

Forex •

Crypto •

Indices •

Stocks •

Commodities

One timing model. Multiple markets

REAL-TIME

Live timing research available directly on the website.

CURRENTLY AVAILABLE:

and more instruments (soon)

Trade Time. Not Price.

Learn moreOfficial VISTmany overview — Watch on YouTube